If you are wondering what happens to credit card debts when you pass away, you've come to the right place. This article will discuss Unsecured and Statute of limitations for pursuing debts after your death. It also addresses if a debt can be transferred or reinstated after you pass away.

If you're not able to pay the debt, it's impossible to pursue unsecured creditors.

Unsecured debts that you have left behind are not usually pursued by creditors after your death. Because they aren't secured against your home or any other assets, unsecured debts cannot be pursued by creditors after you die. Creditors can't take them as soon as you die. Instead, they will wait until you have settled your priority debts such credit cards or loans. Advertise in your local newspaper and you can help creditors find the debts.

The most common type of unsecured debts include credit card debt, personal loan debt, and more. Your estate can pay unsecured debts after your death. In states where the debts have been secured by property, however, the estate is not required to repay them.

Unsecured debts may be transferred or reinstated upon death

After a person passes away, their family may be left to deal with unpaid credit card debt. Although the estate typically pays the debt, there are some exceptions. Often, a joint account or certain state laws will prevent the creditor from being able to collect after a person has passed away. You should notify credit card companies immediately and ensure that all financial documentation is organized.

Because they are not secured by collateral, unsecured credit card debts can be the most difficult to transfer. Creditors may contact the surviving inheritors to collect the debt. It is important to consult a lawyer in such cases. An experienced attorney will be able to organize all necessary documents and give advice about the best sequence of debt payments. Do not allow creditors to seize assets from your loved ones and then use them to collect your debts.

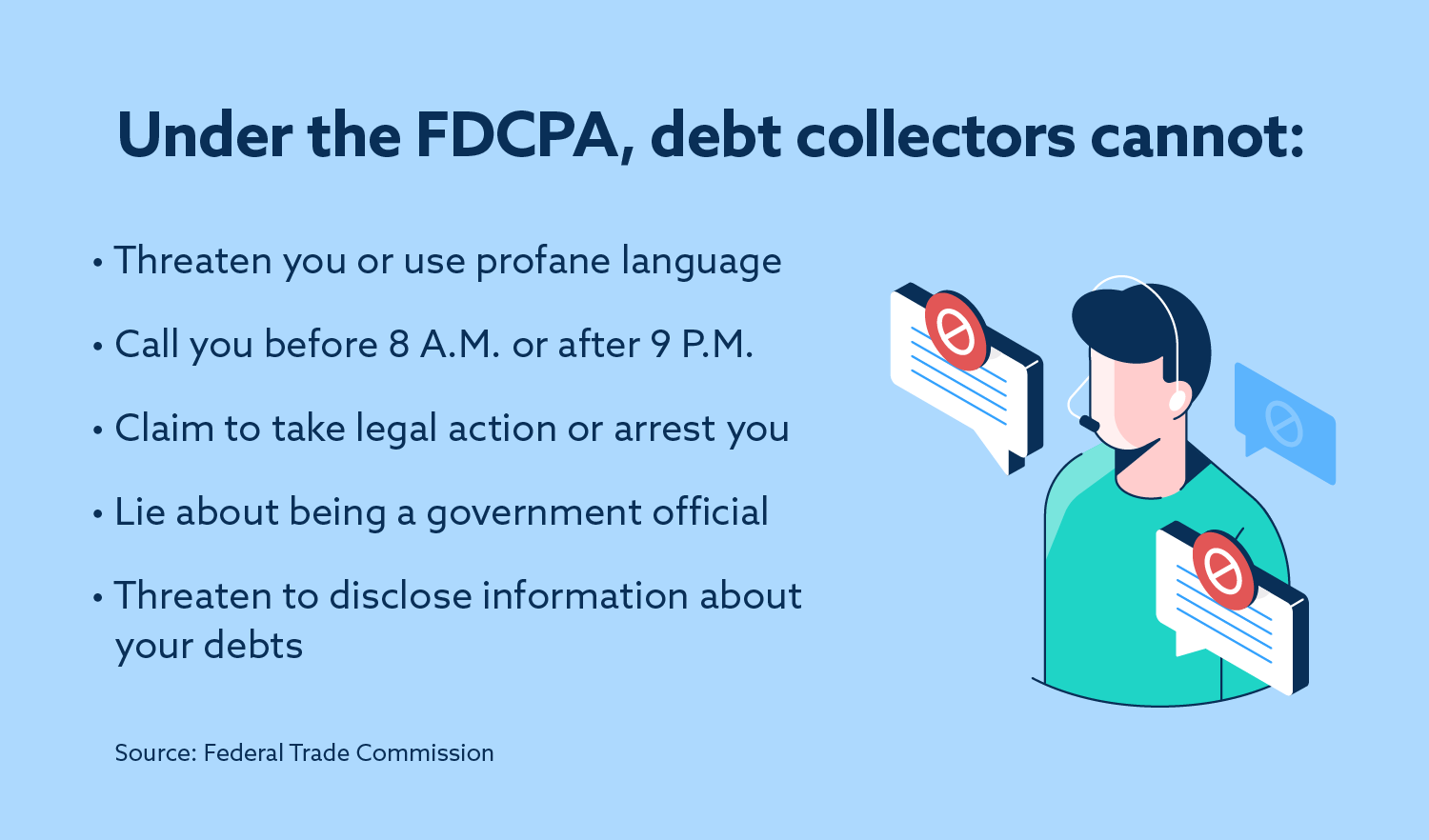

Statute of limitations for collecting uncollectible debts upon death

There are certain limitations that creditors must follow after the death of the decedent, regardless of type of credit cards debt. Unsecured credit cards have a statute for limitations. This starts when the estate executor informs credit card companies that the deceased has died. In some states, the deadline is as short as a few months. California Code of Civil Procedure Section 366.2, for example, sets out the deadlines for creditors to seek payment after the death of a decedent.

To collect the debt, the creditor may have to show that the debt is not barred by law in certain cases. If you think that the debt is statute barred, you should explain this in your correspondence with the creditor. Citizens Advice can help you if you are unsure how to write the letter. You can also contact Citizens Advice to help you write the letter. In certain cases, they will look into your complaint. It is possible to call the Financial Ombudsman using a mobile or landline telephone.

After a death, credit freeze

The credit freeze can help prevent unauthorised transactions on the deceased's credit record. Notifying credit bureaus about the death is the best way to do this. It could take several weeks for the bureaus approval of your request. You should still request the credit report of the deceased from each bureau. This will prevent fraud on the deceased's account, and it will also help you to identify unpaid debts.

Once you have identified the deceased's creditors, you can request copies of their credit reports from each bureau. To find any unpaid accounts, you should carefully review these files. Contact these lenders and creditors to make any necessary changes.

Avoiding identity theft after a death

It can be very difficult for a family to avoid identity theft after a passing. This will save them a lot in financial and emotional distress. Identity thieves can easily steal a person's identity. They may find important personal information in public records, such as financial records, financial records, obituaries, death certificates, divorce certificates, marriage certificates, and divorce certificates. Many identity thieves use these records to create a fake identity and get loans and services.

It is possible to prevent identity thieves stealing your loved one's identity. This is important as identity thieves will have ample time to steal personal information from the deceased and open accounts with that information. Notify the credit bureaus about the death to prevent it from happening and ask them to flag the account with a "deceased” note.

FAQ

Which side hustles are the most lucrative in 2022

You can make money by creating value for someone else. If you do this well, the money will follow.

While you might not know it, your contribution to the world has been there since day one. As a baby, your mother gave you life. The best place to live was the one you created when you learned to walk.

You'll continue to make more if you give back to the people around you. Actually, the more that you give, the greater the rewards.

Without even realizing it, value creation is a powerful force everyone uses every day. Whether you're cooking dinner for your family, driving your kids to school, taking out the trash, or simply paying the bills, you're constantly creating value.

Today, Earth is home for nearly 7 million people. Each person creates an incredible amount of value every day. Even if your hourly value is $1, you could create $7 million annually.

If you could find ten more ways to make someone's week better, that's $700,000. Think about that - you would be earning far more than you currently do working full-time.

Let's suppose you wanted to increase that number by doubling it. Let's suppose you find 20 ways to increase $200 each month in someone's life. You would not only be able to make $14.4 million more annually, but also you'd become very wealthy.

There are millions of opportunities to create value every single day. This includes selling ideas, products, or information.

Although many of us spend our time thinking about careers and income streams, these tools are only tools that enable us to reach our goals. Helping others to achieve their goals is the ultimate goal.

Create value to make it easier for yourself and others. Use my guide How to create value and get paid for it.

How to build a passive stream of income?

To generate consistent earnings from one source, you have to understand why people buy what they buy.

Understanding their needs and wants is key. It is important to learn how to communicate with people and to sell to them.

You must then figure out how you can convert leads into customers. To keep clients happy, you must be proficient in customer service.

Although you might not know it, every product and service has a customer. If you know the buyer, you can build your entire business around him/her.

To become a millionaire it takes a lot. It takes even more work to become a billionaire. Why? Because to become a millionaire, you first have to become a thousandaire.

You can then become a millionaire. You can also become a billionaire. The same goes for becoming a billionaire.

How does one become billionaire? You must first be a millionaire. You only need to begin making money in order to reach this goal.

You must first get started before you can make money. Let's look at how to get going.

What is the difference between passive income and active income?

Passive income is when you earn money without doing any work. Active income requires effort and hard work.

When you make value for others, that is called active income. If you provide a service or product that someone is interested in, you can earn money. Selling products online, writing ebooks, creating websites, and advertising your business are just a few examples.

Passive income is great because it allows you to focus on more important things while still making money. But most people aren't interested in working for themselves. So they choose to invest time and energy into earning passive income.

Passive income doesn't last forever, which is the problem. If you hold off too long in generating passive income, you may run out of cash.

It is possible to burn out if your passive income efforts are too intense. So it's best to start now. If you wait to start earning passive income, you might miss out opportunities to maximize the potential of your earnings.

There are three types or passive income streams.

-

These include starting a business, owning a franchise or becoming a freelancer. You could also rent the property, such as real-estate, to other people.

-

These investments include stocks and bonds as well as mutual funds and ETFs.

-

Real Estate - this includes rental properties, flipping houses, buying land, and investing in commercial real estate

How do rich people make passive income?

If you're trying to create money online, there are two ways to go about it. Another way is to make great products (or service) that people love. This is called "earning” money.

You can also find ways to add value to others, without having to spend your time creating products. This is "passive" income.

Let's assume you are the CEO of an app company. Your job is to create apps. You decide to make them available for free, instead of selling them to users. Because you don't rely on paying customers, this is a great business model. Instead, you can rely on advertising revenue.

You might charge your customers monthly fees to help you sustain yourself as you build your business.

This is how internet entrepreneurs who are successful today make their money. They are more focused on providing value than creating stuff.

How much debt can you take on?

It is vital to realize that you can never have too much money. You will eventually run out money if you spend more than your income. Because savings take time to grow, it is best to limit your spending. Spend less if you're running low on cash.

But how much is too much? There's no right or wrong number, but it is recommended that you live within 10% of your income. You'll never go broke, even after years and years of saving.

This means that even if you make $10,000 per year, you should not spend more then $1,000 each month. You shouldn't spend more that $2,000 monthly if your income is $20,000 For $50,000 you can spend no more than $5,000 each month.

Paying off your debts quickly is the key. This includes student loans and credit card bills. You'll be able to save more money once these are paid off.

You should consider where you plan to put your excess income. If you choose to invest your money in bonds or stocks, you may lose it if the stock exchange falls. If you save your money, interest will compound over time.

For example, let's say you set aside $100 weekly for savings. That would amount to $500 over five years. After six years, you would have $1,000 saved. You would have $3,000 in your bank account within eight years. In ten years you would have $13,000 in savings.

At the end of 15 years, you'll have nearly $40,000 in savings. Now that's quite impressive. You would earn interest if the same amount had been invested in the stock exchange during the same period. Instead of $40,000, you'd now have more than $57,000.

It's crucial to learn how you can manage your finances effectively. If you don't do this, you may end up spending far more than you originally planned.

What is personal finance?

Personal finance involves managing your money to meet your goals at work or home. It is about understanding your finances, knowing your budget, and balancing your desires against your needs.

If you master these skills, you can be financially independent. This means you are no longer dependent on anyone to take care of you. You don't need to worry about monthly rent and utility bills.

Not only will it help you to get ahead, but also how to manage your money. You'll be happier all around. When you feel good about your finances, you tend to be less stressed, get promoted faster, and enjoy life more.

What does personal finance matter to you? Everyone does! Personal finance is one of the most popular topics on the Internet today. Google Trends reports that the number of searches for "personal financial" has increased by 1,600% since 2004.

People use their smartphones today to manage their finances, compare prices and build wealth. These people read blogs like this one and watch YouTube videos about personal finance. They also listen to podcasts on investing.

In fact, according to Bankrate.com, Americans spend an average of four hours a day watching TV, listening to music, playing video games, surfing the Web, reading books, and talking with friends. This leaves just two hours per day for all other important activities.

Personal finance is something you can master.

Statistics

- Mortgage rates hit 7.08%, Freddie Mac says Most Popular (marketwatch.com)

- As mortgage rates dip below 7%, ‘millennials should jump at a 6% mortgage like bears grabbing for honey' New homeowners and renters bear the brunt of October inflation — they're cutting back on eating out, entertainment and vacations to beat rising costs (marketwatch.com)

- According to the company's website, people often earn $25 to $45 daily. (nerdwallet.com)

- Shares of Six Flags Entertainment Corp. dove 4.7% in premarket trading Thursday, after the theme park operator reported third-quarter profit and r... (marketwatch.com)

- Etsy boasted about 96 million active buyers and grossed over $13.5 billion in merchandise sales in 2021, according to data from Statista. (nerdwallet.com)

External Links

How To

How to Make Money from Home

There is always room for improvement, no matter what online income you have. Even the most successful entrepreneurs can struggle to grow and increase profits.

The problem with starting a business is that it's easy for you to get stuck in a routine and not focus on your goals. You may spend more time on marketing rather than product development. Or you may neglect customer service altogether.

It is important to evaluate your progress periodically and ask yourself if you are improving or maintaining your status quo. If you're ready to boost your income, consider these five ways.

Productivity doesn't only revolve around the output. You also have to be able to accomplish tasks effectively. Delegate those parts to someone else.

You could, for example, hire virtual assistants to manage your social media, email administration, and customer service.

Another option is to design blog posts for one team member and another person to manage lead-generation efforts. Delegating should be done with people who will help you accomplish your goals quicker and better.

-

Focus on Sales instead of Marketing

Marketing doesn't mean spending a lot. Some of the best marketers aren't paid employees at all. They are self-employed and make a living as consultants.

Instead of advertising on TV, radio, or print ads, you can look into affiliate programs, which allow you promote other companies' products and/or services. For sales to be generated, you don’t need to buy expensive inventory.

-

Hiring an Expert to Do What you Can't

Freelancers can be hired to fill in the gaps if you don't have enough expertise. A freelance designer could be hired to help you develop graphics for your site, if, for example, you don't know much about graphic design.

-

Get Paid Faster By Using Invoice Apps

Invoicing can be time-consuming when you're a contractor. Invoicing can be especially difficult if you have multiple clients that want different things.

FreshBooks and Xero are two apps that make it simple to invoice customers. All your client information can be entered once and invoices sent directly from the app.

-

Sell More Products With Affiliate Programs

Affiliate programs are great because you can sell products without stock. You don't have to worry about shipping costs. You only need to create a link between your site and the vendor's website. Then, you receive a commission whenever someone buys something from the vendor. Affiliate programs not only help you make more money but they can also help you build your brand. You can attract your audience as long you provide quality content.